》Check SMM aluminum product quotes, data, and market analysis

》Subscribe to view historical spot prices of SMM metals

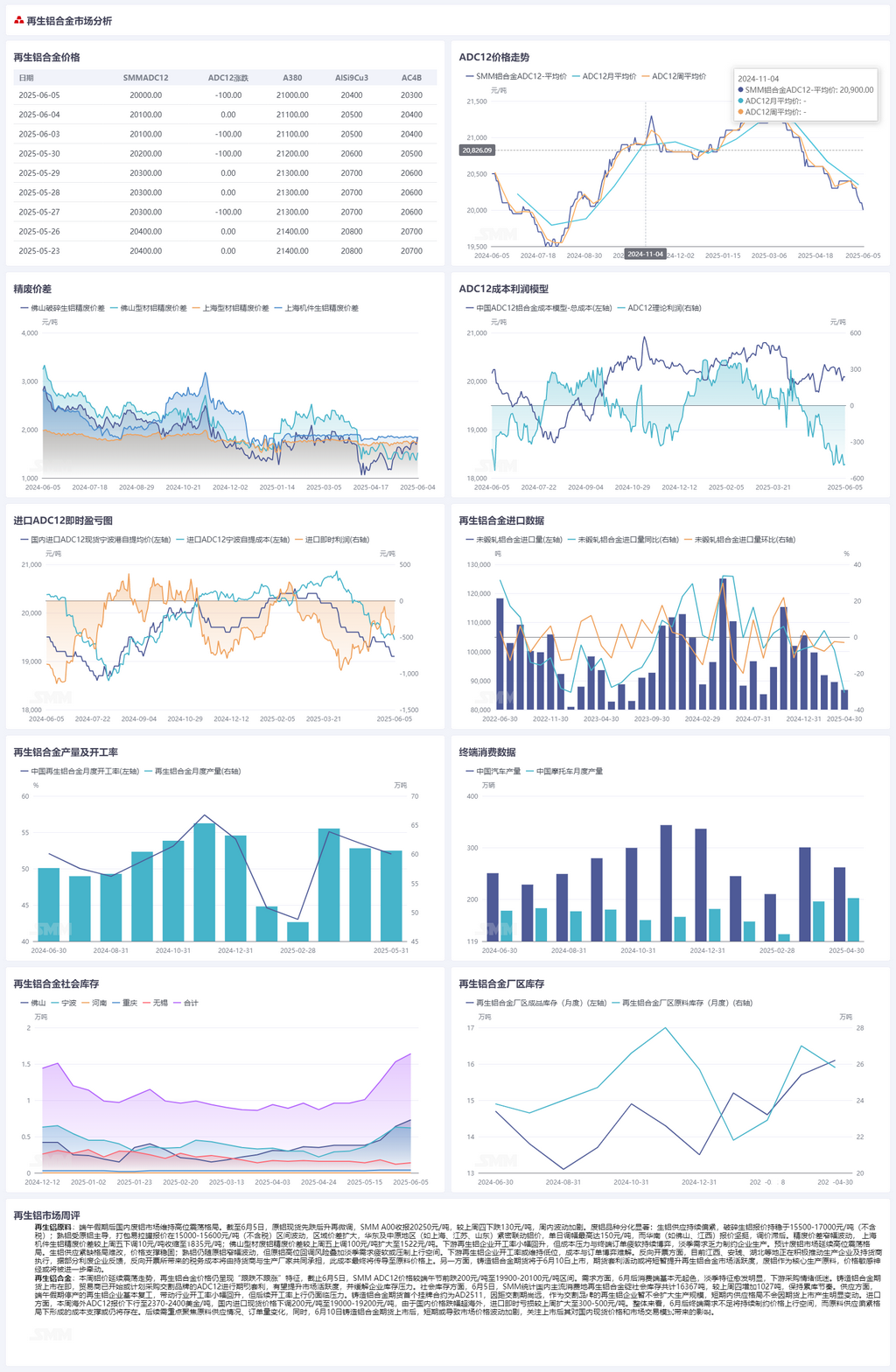

Secondary aluminum raw materials:

After the Dragon Boat Festival holiday, the domestic aluminum scrap market maintained a pattern of fluctuating at highs. As of June 5, spot primary aluminum prices first fell, then rose, and finally adjusted slightly. SMM A00 aluminum ingot prices closed at 20,250 yuan/mt, down 130 yuan/mt from last Thursday, with intensified fluctuations during the week. The differentiation among aluminum scrap varieties was significant: the supply of aluminum tense scrap remained tight, with shredded aluminum tense scrap quotes holding steady at 15,500-17,000 yuan/mt (tax excluded). Wrought aluminum alloy scrap, influenced by primary aluminum, saw baled UBC quotes fluctuating within the 15,000-15,600 yuan/mt range (tax excluded), with regional price differences widening. East China and central China regions (such as Shanghai, Jiangsu, and Shandong) closely tracked aluminum prices, with daily adjustments reaching up to 150 yuan/mt. In contrast, south China (such as Foshan and Jiangxi) maintained firm quotes with delayed price adjustments. The price difference between A00 aluminum and aluminum scrap fluctuated rangebound. The price difference between A00 aluminum and mechanical casting aluminum scrap in Shanghai narrowed by 10 yuan/mt from last Friday to 1,835 yuan/mt. The price difference between A00 aluminum and aluminum extrusion scrap in Foshan widened by 100 yuan/mt from last Friday to 1,522 yuan/mt. The operating rate of downstream secondary aluminum enterprises rebounded slightly, but the ongoing tug-of-war between cost pressure and weak terminal orders, coupled with sluggish off-season demand, constrained enterprise production.

It is expected that the aluminum scrap market will continue to fluctuate at highs. The tight supply of aluminum tense scrap is unlikely to change, providing solid price support. Wrought aluminum alloy scrap will continue to fluctuate rangebound with primary aluminum, but the risk of a high-level correction in primary aluminum prices, combined with weak off-season demand, may suppress upside room. The operating rate of downstream secondary aluminum enterprises may remain low, with the tug-of-war between costs and orders remaining unresolved. Regarding reverse invoicing, Jiangxi, Anhui, Hubei, and other regions are actively promoting its implementation among producers and suppliers. According to feedback from some scrap utilisation enterprises, the tax costs arising from reverse invoicing will be shared by suppliers and producers, and these costs will ultimately be passed on to raw material prices. On the other hand, cast aluminum alloy futures will be listed on June 10. Futures arbitrage activities may temporarily boost market activity in the secondary aluminum alloy market. As aluminum scrap is a core production raw material, its price sensitivity may be further heightened.

Secondary aluminum alloy:

This week, aluminum prices continued to fluctuate, with secondary aluminum alloy prices still exhibiting the characteristic of "following declines but not increases." As of June 5, SMM ADC12 prices fell by 200 yuan/mt from before the Dragon Boat Festival to the 19,900-20,100 yuan/mt range. On the demand side, there has been little improvement in the consumption end since June, with off-season characteristics becoming increasingly pronounced and downstream procurement sentiment remaining low. With the upcoming listing of cast aluminum alloy futures, traders have already started or plan to purchase ADC12 of delivery brands for futures-spot arbitrage, which is expected to boost market activity and alleviate enterprise inventory pressure. In terms of social inventory, on June 5, SMM reported that the total social inventory of secondary aluminum alloy ingots in major domestic consumption areas was 16,367 mt, an increase of 1,027 mt from the previous Thursday, maintaining the inventory buildup trend. In terms of supply, secondary aluminum producers that halted operations during the Dragon Boat Festival holiday have largely resumed production, driving a slight rebound in the industry's operating rate. However, there is still pressure on the operating rate to rise further. The first listed contract for cast aluminum alloy futures is AD2511. Given the long time until delivery, secondary aluminum producers, which are delivery brands, will not expand production scale for the time being. In the short term, the supply landscape will not change significantly due to the listing of futures. In terms of imports, overseas ADC12 quotes fell to USD 2,370-2,400/mt this week, while domestic import spot prices dropped by 200 yuan/mt to 19,000-19,200 yuan/mt. As domestic prices fell more sharply than overseas prices, the immediate import loss expanded to 300-500 yuan/mt WoW. Overall, insufficient end-use demand after June will continue to constrain the upside room for prices, while cost support formed under the tight supply of raw materials may still exist. Going forward, it is necessary to focus on the raw material supply situation and changes in orders. Meanwhile, after the listing of cast aluminum alloy futures on June 10, it may lead to increased short-term market price volatility. Attention should be paid to the impact of the listing on domestic spot prices and market trading patterns.